How Social Security Benefits Work

Social Security calculates your benefit based on your 35 highest-earning years of work history (adjusted for inflation). The result is your Primary Insurance Amount (PIA) — the monthly benefit you'd receive if you claim at your Full Retirement Age (FRA).

Your FRA depends on your birth year:

- Born 1943–1954: FRA is 66

- Born 1955–1959: FRA is 66 and 2–10 months

- Born 1960 or later: FRA is 67

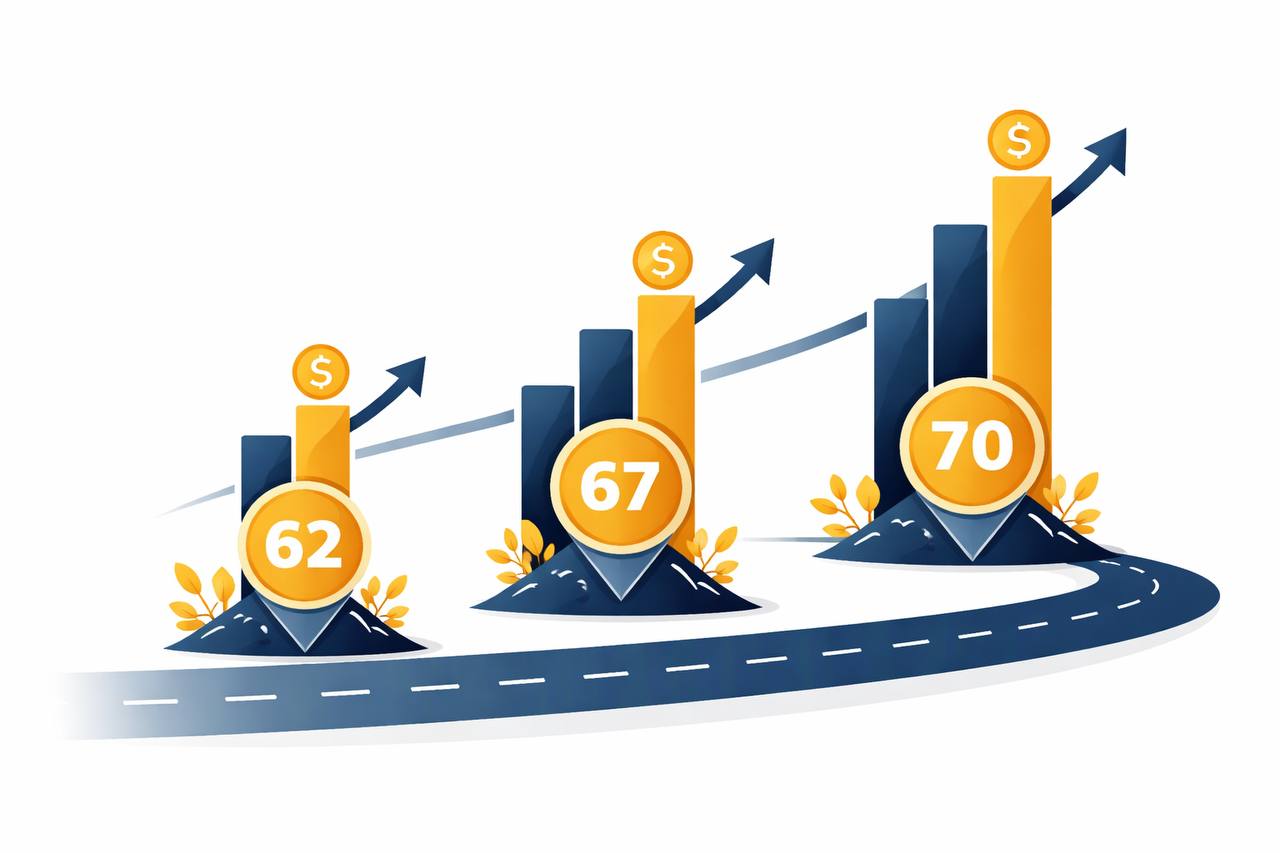

You can claim benefits as early as 62 or as late as 70. Every month you delay changes your benefit amount permanently.

The Impact of Your Claiming Age

If your Full Retirement Age is 67 and your PIA is $2,000/month, here's what happens when you claim at different ages:

- Age 62: ~$1,400/month (30% reduction — maximum reduction)

- Age 64: ~$1,600/month (20% reduction)

- Age 66: ~$1,867/month (6.7% reduction)

- Age 67 (FRA): $2,000/month (full benefit)

- Age 68: $2,160/month (+8%)

- Age 70: $2,480/month (+24% — maximum benefit)

For each year you delay past FRA, your benefit increases by 8% — that's a guaranteed, risk-free 8% return that's hard to beat elsewhere.

The Break-Even Analysis

The key question: if you claim early and receive more payments, but each payment is smaller, when does waiting pay off?

Comparing claiming at 62 vs. 67 (FRA): You receive 60 extra months of benefits at $1,400 = $84,000 total before age 67. After 67, the person who waited gets $600/month more. Break-even point: $84,000 ÷ $600 = 140 months after FRA, or roughly age 78.5.

Comparing claiming at 67 vs. 70: Waiting 36 months means 36 × $2,000 = $72,000 foregone. After 70, the person who waited gets $480/month more. Break-even: $72,000 ÷ $480 ≈ 150 months after age 70, or age 82.5.

Key insight: If you expect to live past about 80–82, delaying Social Security to 70 almost always wins in terms of total lifetime income. The Social Security Administration reports that average life expectancy for a 65-year-old today is approximately 85 for men and 87 for women — well past the break-even point.

Reasons to Claim Early (62–65)

Despite the math favoring delay, early claiming makes sense in some situations:

- Poor health or shortened life expectancy: If you have reason to believe you won't reach your mid-80s, early claiming maximizes total lifetime income.

- Immediate financial need: If you have no other income source and genuinely need the money, claiming early is better than taking on high-interest debt.

- High-earning spouse who will delay: If your spouse has higher lifetime earnings and will delay to 70, your combined household strategy may support you claiming early.

- Continuing to work with limited income: Careful — before FRA, Social Security reduces benefits if you earn over $22,320/year (2025 limit). But those "withheld" benefits are added back after FRA.

Reasons to Delay (Especially to 70)

- Longevity: If long lifespans run in your family, delay maximizes lifetime income.

- Low other savings: Social Security is inflation-adjusted and guaranteed for life. If your savings are modest, a higher guaranteed income is extremely valuable.

- Surviving spouse protection: When one spouse dies, the survivor receives the higher of the two benefits. The higher earner delaying to 70 creates maximum survivor protection.

- Health insurance bridge: If you have employer coverage or can afford ACA coverage until Medicare at 65, delaying Social Security fits naturally.

Spousal and Survivor Benefits

Social Security's spousal benefit rules add complexity — and planning opportunity:

- A spouse can claim up to 50% of their partner's FRA benefit (while both are living)

- Survivor benefits equal up to 100% of the deceased spouse's benefit (including delayed credits)

- If the higher earner delays to 70 and dies first, the surviving spouse receives that higher amount for life

- You can claim a spousal benefit as early as 62 (with reductions)

For couples, Social Security claiming strategy is a combined optimization problem. Tools like the free SSA online calculator and professional Social Security optimization software can help model your specific situation.

Working While Receiving Social Security

Before your Full Retirement Age, earning income above the threshold ($22,320 in 2025) will temporarily reduce your Social Security benefits — $1 withheld for every $2 earned above the limit. These are not "lost" — they're credited back to you as an increase after you reach FRA.

At and after FRA, you can earn unlimited income with no reduction in benefits. If you plan to continue working, reaching FRA before claiming is cleaner.

🧮 Model Your Social Security in the Retirement Calculator

Enter your estimated Social Security benefit in our advanced calculator to see how different claiming ages affect your overall retirement picture.

Open Advanced Calculator →Close to retirement?

Compare timing decisions on our Can I Retire at 65? page and then run your own scenario.

How to Get Your Social Security Estimate

- Visit ssa.gov/myaccount and create a my Social Security account

- View your earnings history and projected benefits at 62, FRA, and 70

- Verify your earnings history is accurate — errors happen and they affect your benefit

- Use the SSA's Retirement Estimator for different scenarios

The online estimate assumes you continue working at your current salary until claiming age. If you plan to retire before claiming, download your earnings record and use the actual calculation.

Frequently Asked Questions

Sources & References

- SSA.gov — my Social Security Account — Official portal to view your personal Social Security statement and benefit estimates

- SSA — Retirement Benefits Estimator — Official tool for estimating your retirement benefit at various claiming ages

- Social Security Administration — "When to Start Receiving Retirement Benefits" — Official SSA publication on early vs. delayed claiming tradeoffs

- SSA — Fast Facts & Figures About Social Security — Annual statistical reference including average benefit amounts and demographic data